Different Forms, Same Function, But Abiding By Identical Limits

The Dude abides.

The Dude, from The Big Lebowski

We’ve seen it over and over again.

A new product is entering the market, and everyone who helped bring it to life believes it will revolutionize the industry. And, with respect to its Value (i.e., its sustainable price based on its features), they often do.

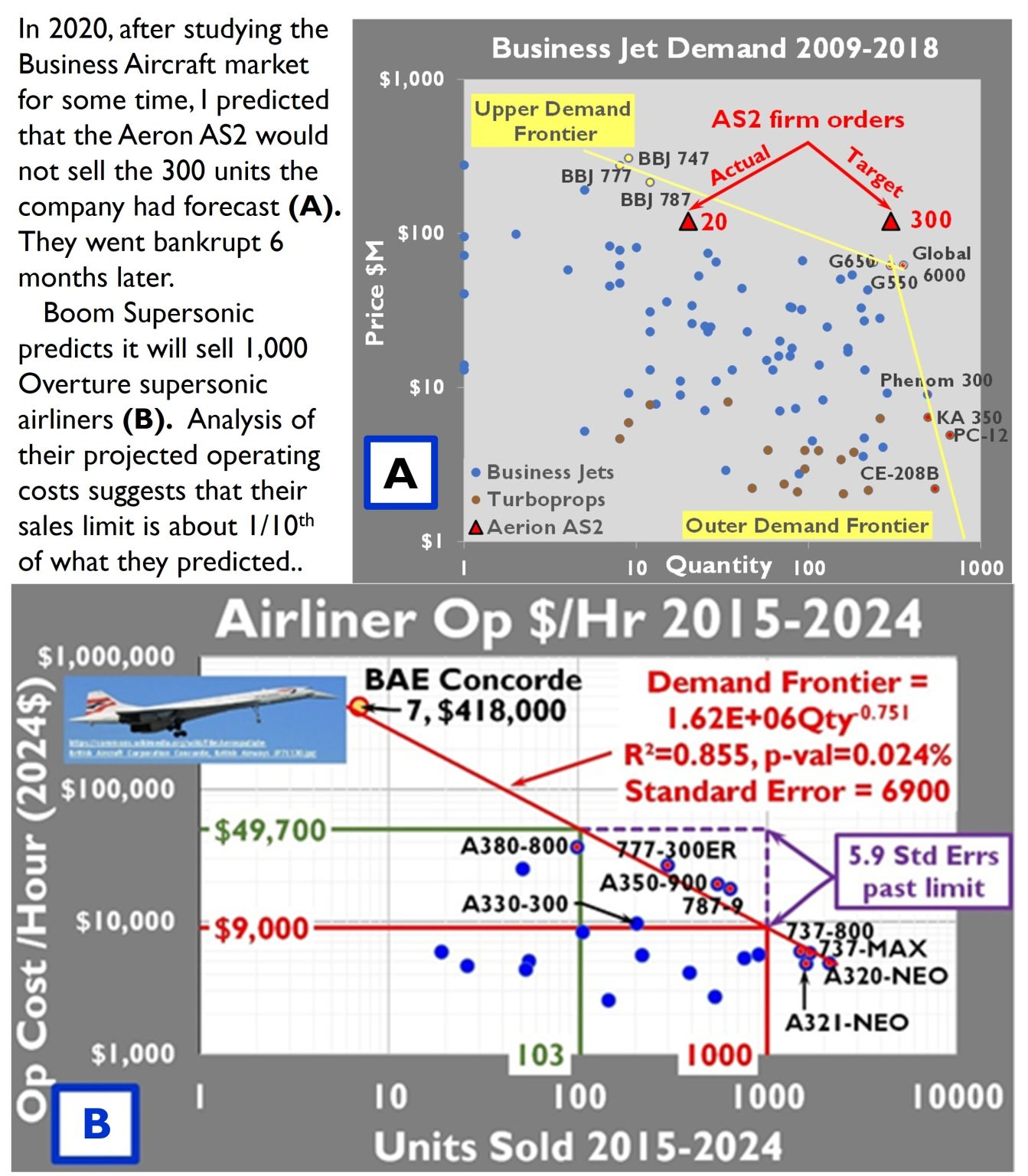

The supersonic Concorde sold for $46M (in 1977), compared to the subsonic McDonnell Douglas DC-9 ($7.6M in 1977), which carried the same number of passengers.

The hypersonic AGM-183A missile, at $42M (2016$), costs more than the high subsonic AGM-158-1 JASSM-ER, at $1.9M (2016$).

The Concorde was projected to sell 350 units. They sold 14. Meanwhile, the DC-9 sold 976 units.

The Congressional Budget Office saw a market for 300 AGM-183As. One was sold. The JASSM-ER has sold 3360 units to date.

In both cases, the Demand Curves weren’t broken. They were instead ignored. Had those curves in those timeframes been properly characterized, neither program should have launched.

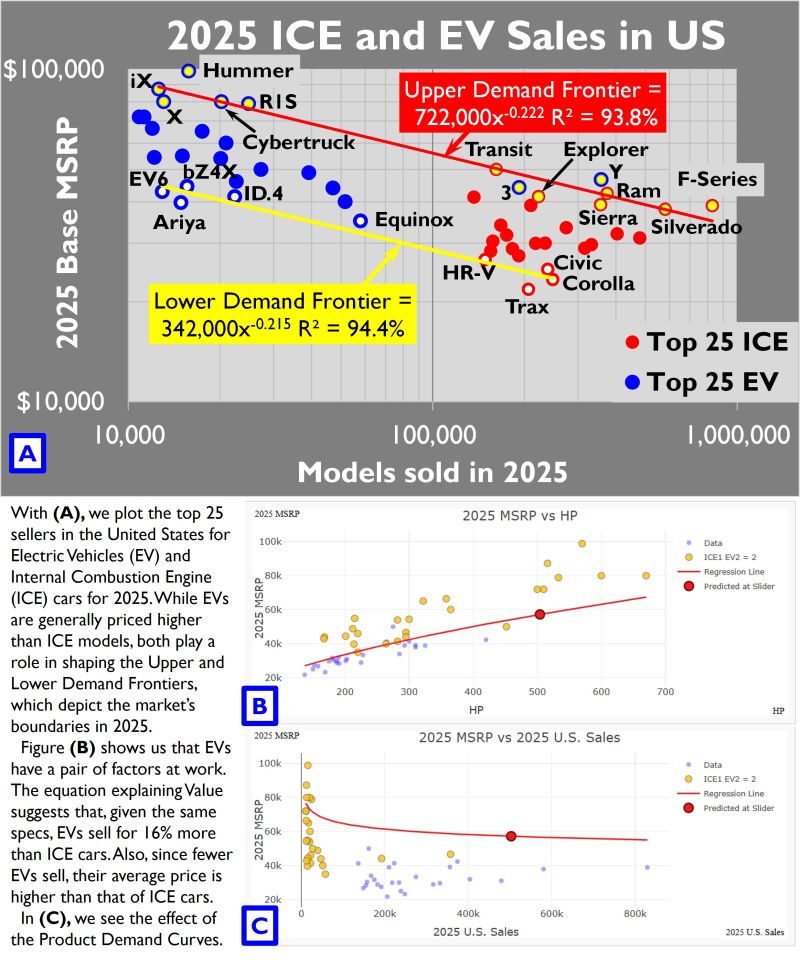

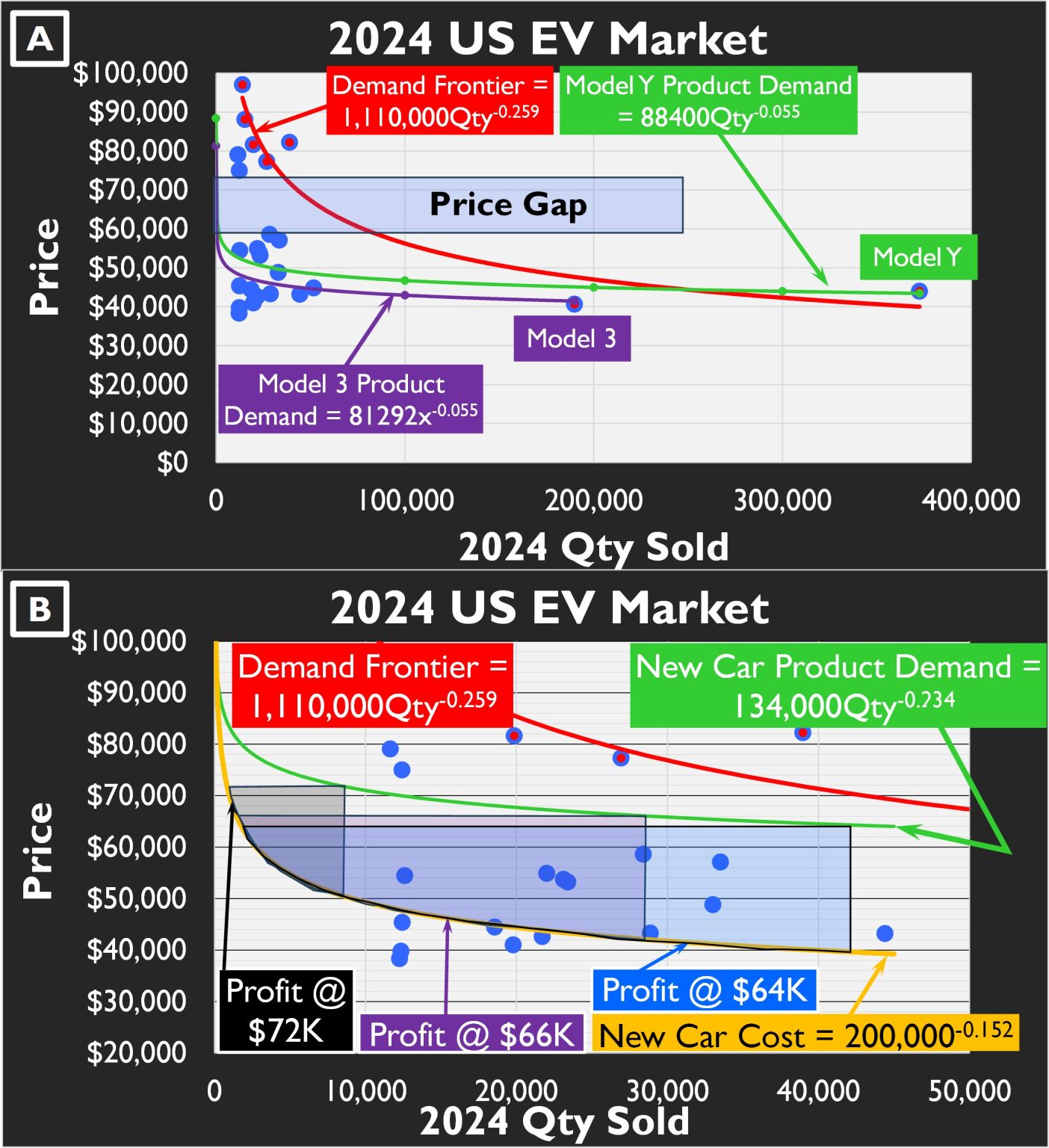

At the beginning of the modern era of mass-produced electric cars, many saw the market as brand-new.

But, as we see in Figure (A) below, while the top 25 sellers of Electric Vehicles (EVs) in the US command higher prices than the top 25 Internal Combustion Engine (ICE) vehicles, both are bound by the same Demand Limits. At the lower end of the market, a group of EVs (EV6, Ariya, Equinox, etc.) joins a similar group of ICE machines (including the Trax, Corolla, and Civic) to form the Lower Demand Frontier. The Upper Demand Frontier is formed by, among others, EVs such as the Tesla X and Hummer at the high end, and the Model 3 and Y at the low end, with familiar ICE market leaders, Ram, Sierra, and the F-Series.

The ability of the Models 3 and Y to sell so many models is both a testament to Tesla’s low costs, along with the market’s overall Value proposition, which, for the 50 models studied, is:

2025 MSRP = 3780*HP^0.574 * ICE1 EV2^0.211 * 2025 U.S. Sales^-0.076

The Sales Term (U.S. Sales-0.076) rounds to the equivalent of a 95% Product Demand Curve. At the same time, the industry typically demonstrates an 85% Learning Curve. Thus, Prices will not fall as fast as costs, meaning that the overall Upper Demand Frontier forms the market limit.

With the Lower and Upper Demand Frontier slopes of -0.22, the market offers far more money at its lower end than at higher prices. Will these slopes continue at the same rate if new, low-cost machines are added to the lower end of the market, or will the market experience steep downward breaks in its Demand Frontiers, as we’ve seen in Business and General Aviation aircraft, revealing that the market has reached saturation?

Designers of the next model entering the automotive market must understand its limits.

The Dude abides.

You should, too.

#evs #ice #hypernomics #demand